INDUSTRY TRENDS

Alabama Just Enforced Its PBM Law. The Rest of the Country Is Watching

Alabama Just Enforced Its PBM Law. The Rest of the Country Is Watching

Alabama Just Enforced Its PBM Law. The Rest of the Country Is Watching

Alabama Just Enforced Its PBM Law. The Rest of the Country Is Watching

I got a call from a pharmacy owner in Birmingham last week. She was excited. I mean, genuinely, can't-contain-it excited. "Did you see what Alabama did?" she asked. "The state actually went after Express Scripts."

That call stays with me because it represents something that feels new in the pharmacy advocacy world. For years, we've talked about PBM reform as a distant policy goal. Something that's necessary but maybe not achievable in our lifetime. Something that felt like pushing against a wall that never moved.

And then Alabama moved the wall.

On October 1, 2025, Alabama's Community Pharmacy Relief Act became effective. And just a few months later, the state's newly established PBM Compliance Division did something unprecedented: it issued an enforcement action against Express Scripts, one of the three largest pharmacy benefit managers in the United States. This isn't theoretical. This isn't advocacy-speak. This is a state government with enforcement power following through on what it promised. And for independent pharmacies watching from every other state, the message is clear: PBM reform is possible. And the template for how to do it is right here.

What Alabama Actually Did (And Why It Was Necessary)

Let me start with the law, because understanding what Alabama prohibited is the best way to understand what was broken before.

Alabama's Community Pharmacy Relief Act, formally SB 252, addresses four core problems that have plagued independent pharmacies for years.

First, the law prohibits PBMs from reimbursing independent pharmacies below the Medicaid reimbursement rate. This is the spread pricing problem in statute form. Spread pricing is when a PBM reimburses a pharmacy at one rate but bills the insurance plan or patient at a higher rate, pocketing the difference. It's a practice that exists nowhere except between PBMs and pharmacies. Hospitals don't do it to their suppliers. Insurance companies don't do it to their networks. But PBMs do it to pharmacies, and it's been legal for years. Alabama said: not anymore, at least not for rates below Medicaid.

Second, the law explicitly prohibits steering. Steering is when a PBM directs patients away from a particular pharmacy (often an independent) toward another pharmacy (often a chain or a mail-order operation the PBM owns). Steering is dressed up in language about "network optimization" or "patient convenience," but what it actually means is the PBM chooses which pharmacies succeed and which ones fail based on the PBM's financial interests, not the patient's interests.

Third, Alabama requires 100% rebate pass-through to health benefit plan clients. Rebates are money that drug manufacturers pay to PBMs, supposedly in exchange for formulary placement. The problem is that PBMs have been keeping rebates and not passing them through to the plans that should benefit, which means patients and employers still pay the list price. A requirement for 100% pass-through means the insurance plans and patients actually get the benefit of the rebates that manufacturers are paying for.

And fourth, the law prevents PBMs from denying network participation to pharmacies or retaliating against pharmacies that exercise their legal rights. This sounds vague until you understand that PBMs have historically used network participation as a means of leverage. Pharmacy doesn't accept a lowball reimbursement rate? PBM removes it from the network. Pharmacy joins a trade association that advocates for higher reimbursement? PBM retaliates. Pharmacy sues over underpayment? PBM kicks it off the network. Alabama said: this has to stop.

Each of these provisions addresses a real problem. But here's what matters: Alabama actually enforced them.

The First Enforcement Action (And What It Reveals)

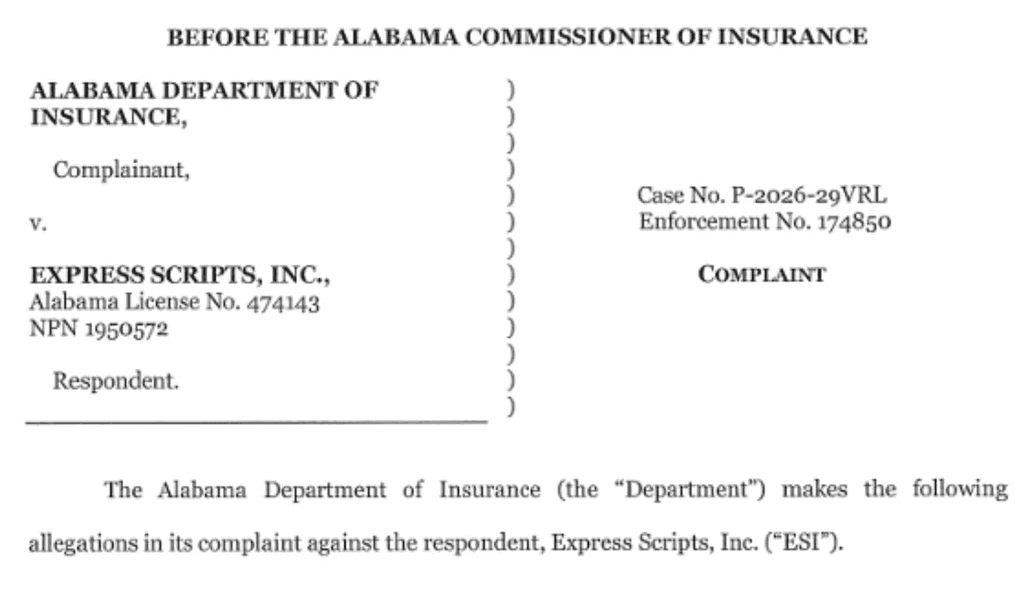

In early 2026, Alabama's PBM Compliance Division, under the supervision of the Department of Insurance, issued a finding against Express Scripts. This was the first enforcement action of its kind in the United States.

The violations were specific. Express Scripts was charging pharmacies illegal fees that weren't part of their network agreements. It was reimbursing pharmacies at rates below the Medicaid reimbursement rate for commercial patients, which is explicitly prohibited by the law. And it was being consistently unresponsive to department inquiries, which is its own kind of violation: if the regulator can't get answers, it can't do its job.

Now here's what I find most important about this enforcement action. It wasn't theoretical. It wasn't based on a formal complaint that the state then spent three years investigating. It was a fairly direct regulatory action based on what the Department of Insurance could observe happening in the marketplace. The state said, "We see the problem. We're enforcing the law. Stop."

Express Scripts doesn't have a mechanism to appeal to a higher authority that might side with the PBM. The law is clear. The violation was documented. The state enforced it.

This changes the incentive structure for PBMs, at least in Alabama. If you violate the law, the regulator will catch you and you'll have to correct the behavior. That's not guaranteed everywhere, but it's guaranteed in Alabama now.

Why This Matters Nationally (And It Really Does)

Here's the part that keeps pharmacy owners awake at night in a good way: this enforcement action creates a template.

For years, PBM reform has been something that pharmacy advocates have talked about in abstract terms. "We need legislation that addresses spread pricing." "We need transparency requirements." "We need enforcement mechanisms." These are the policy goals. But translating policy goals into actual enforcement is where most reform efforts die. The law gets passed, but the regulator doesn't have resources, or appetite, or clarity about how to enforce it. So the law sits on the books and the PBM practices continue.

Alabama proved that this doesn't have to happen. You can write a clear law, establish a compliance division, give that division a mandate to enforce, and actually hold PBMs accountable when they violate. The state didn't need to invent a new regulatory apparatus. It used existing state infrastructure (the Department of Insurance) and gave it a specific focus.

This is replicable. Every state has an Insurance Department. Every state has the legal authority to regulate the entities operating within its borders. Alabama just showed other states how to use that authority.

The national momentum is already building. Other states are watching this. Tennessee is considering similar legislation. Several states are in conversations about what Alabama's law actually accomplished. The pharmacy advocacy world is seeing this as proof that reform isn't just possible, it's achievable in timeframes that matter for business. Not someday. Now.

But here's what matters most: this puts competitive pressure on PBMs. If Alabama enforces its law and Express Scripts has to adjust its behavior in Alabama, it affects Express Scripts' profit model nationwide. PBMs operate with uniform systems across all states. If they can't engage in spread pricing in Alabama, they're going to face pressure to be more transparent about spread pricing everywhere. If they can't steer in Alabama, they're going to be defending their steering practices in other states.

One state's enforcement action creates pressure that ripples across the entire system.

The Express Scripts Specific Issue (And Why It Matters for Your Relationship)

Let me be direct about what Express Scripts was doing, because it illustrates the problem that PBM regulation is trying to solve.

Express Scripts was charging pharmacies fees that weren't contractually agreed to. This is a common practice. A PBM will charge a pharmacy for services, audits, compliance checks, technology fees, without those fees being in the original network agreement. The pharmacy finds out after the fact that their reimbursement was reduced for reasons they didn't know existed. It's a bait-and-switch dressed up in regulatory language.

Express Scripts was reimbursing pharmacies below the Medicaid rate for commercial prescriptions. This is the spread pricing problem. A pharmacy might be reimbursed $15 for a commercial fill while Medicaid would reimburse $18 for the same prescription from the same pharmacy. That $3 spread is spread pricing, and Alabama law explicitly prohibits it. Express Scripts was doing it anyway.

And Express Scripts was blowing off the state's inquiries. When the Department of Insurance asked for documentation about the fees and the reimbursement rates, Express Scripts didn't respond in a timely manner or didn't respond fully. This is where the enforcement action moved from "here are the violations" to "you're also not cooperating with the regulator."

For your pharmacy, if you're an Express Scripts network pharmacy in Alabama, this enforcement action should change your relationship dynamic. You now have a state regulator who has demonstrated that it will enforce the law against the PBM. That changes your leverage. If Express Scripts tries to charge an illegal fee, you have recourse. You have documentation that the state has already told Express Scripts this is prohibited. You can report violations to the Department of Insurance and there's precedent that the state actually investigates.

This is what real PBM accountability looks like, and it starts with enforcement.

What This Means for Pharmacies Outside Alabama

If you're reading this and you're not in Alabama, you might be thinking, "This is interesting but it doesn't affect me." That would be wrong in two important ways.

First, Alabama's law and enforcement action is a toolkit for your state. If you have a state association, you now have evidence that state-level PBM enforcement is possible. You have a specific law to point to. You have data on what Express Scripts and other PBMs are actually doing in your state. You have a template for regulatory language. You have a state (Alabama) that you can ask for advice on implementation.

The pharmacy advocacy world is starting to organize around this. The National Community Pharmacists Association (NCPA) is using Alabama's precedent to pressure other states to pass similar legislation. State associations are looking at Alabama's specific language and adapting it for their own legislatures. This is how policy change actually happens: one state moves first, then others follow.

Second, the Express Scripts enforcement is setting a precedent about what constitutes reasonable enforcement of PBM law. Any pharmacist or pharmacy owner who's been underpaid by a PBM now has an argument to make to their state regulator. "Alabama's Department of Insurance found that Express Scripts was charging illegal fees and reimbursing below Medicaid rates. Our state should investigate whether the same is happening here."

This is where individual pharmacy action connects to systemic change. Every pharmacy owner who files a complaint with their state insurance commissioner is building the case for why enforcement matters. And now there's precedent that regulators can actually do something about it.

How to Advocate for PBM Reform in Your State Right Now

So what should you do if you're an independent pharmacy owner or a tech who cares about this issue?

First, understand the specific PBM problems in your state. Are you seeing spread pricing? Are you being steered? Are you facing fees that weren't contractually agreed to? Document this. Write it down. The more specific you can be, the more persuasive you are when you talk to your state legislator or your state insurance commissioner.

Second, connect with your state pharmacy association. They're organizing around PBM reform. They probably have legislative priorities for this session. Get involved. Even if you're a tech, not a pharmacy owner, your voice matters in these conversations because you're the person who actually sees what PBMs are doing to the dispensing workflow.

Third, if you're seeing PBM violations, report them to your state insurance commissioner. Include specific documentation. Include dates and amounts when possible. Include how the violation affected your pharmacy's finances or operations. The regulator can only enforce the law if they know the violations are happening.

Fourth, if your state has PBM reform legislation pending, testify if you have the chance. Share your specific story about how PBM practices have affected your pharmacy. Policymakers remember personal stories more than they remember statistics. "The PBM reduced my reimbursement by $50,000 this year through fees I didn't know existed" is more powerful than "PBMs are engaging in spread pricing."

And fifth, think about this as an long-term advocacy effort. Alabama's law didn't happen overnight. It took years of advocacy and relationship-building with legislators. But it happened. And now it's a precedent for other states. Your state's PBM reform is the same thing. It's a long-term effort that you're building toward, even if you don't see the policy change this year or next year.

The Diversified Sourcing Reality

Here’s where I want to be honest about what this means for practice right now.

While you’re advocating for PBM reform in your state, you also need to protect your pharmacy’s margins in the conditions that currently exists. And those conditions are still volatile—between reimbursement pressure, contract unpredictability, and ongoing enforcement actions like Alabama’s recent case against Express Scripts , it’s clear that relying on a single channel for margin is no longer a safe strategy. Even national advocacy groups like NCPA are pointing to Alabama as a signal that enforcement is real—but also that pharmacies need to stay resilient while policy catches up.

One of the most practical ways to do that is to diversify your sourcing.

When you’re dependent on a single PBM reimbursement model or wholesaler contract, you’re exposed to sudden margin compression. This is where modern tools—like pharmacy inventory software and a pharmacy-to-pharmacy marketplace—start to play a much bigger role in day-to-day operations.

Platforms like RxPost allow pharmacies to sell excess pharmacy inventory and source medications directly from other pharmacies. That matters more than ever in a world where shortages are unpredictable and overstock turns into loss overnight. Instead of letting products expire on your shelf, you can convert them into revenue—or access inventory another pharmacy no longer needs. It’s a real, operational drug shortage solution that doesn’t depend on upstream fixes.

And the margin impact is real. When you’re sourcing inventory at a discount from another pharmacy instead of through traditional channels, you’re creating a second, independent lever for profitability—one that isn’t dictated by PBM reimbursement rates.

The long-term strategy is still PBM reform and enforcement, like what Alabama is demonstrating. But the near-term strategy is control—control over your inventory, your sourcing, and your margins.

Because the pharmacies that win in this environment won’t just wait for policy to change.

They’ll build businesses that can survive it.

Take Action While You Advocate for Policy Change

Advocacy takes time. Reform takes longer. In the meantime, protect your pharmacy's margins through smarter sourcing. RxPost connects independent pharmacies with surplus inventory at significant discounts, giving you margin flexibility while you're navigating PBM relationships.

Learn how RxPost helps independent pharmacies diversify sourcing and protect margins

I got a call from a pharmacy owner in Birmingham last week. She was excited. I mean, genuinely, can't-contain-it excited. "Did you see what Alabama did?" she asked. "The state actually went after Express Scripts."

That call stays with me because it represents something that feels new in the pharmacy advocacy world. For years, we've talked about PBM reform as a distant policy goal. Something that's necessary but maybe not achievable in our lifetime. Something that felt like pushing against a wall that never moved.

And then Alabama moved the wall.

On October 1, 2025, Alabama's Community Pharmacy Relief Act became effective. And just a few months later, the state's newly established PBM Compliance Division did something unprecedented: it issued an enforcement action against Express Scripts, one of the three largest pharmacy benefit managers in the United States. This isn't theoretical. This isn't advocacy-speak. This is a state government with enforcement power following through on what it promised. And for independent pharmacies watching from every other state, the message is clear: PBM reform is possible. And the template for how to do it is right here.

What Alabama Actually Did (And Why It Was Necessary)

Let me start with the law, because understanding what Alabama prohibited is the best way to understand what was broken before.

Alabama's Community Pharmacy Relief Act, formally SB 252, addresses four core problems that have plagued independent pharmacies for years.

First, the law prohibits PBMs from reimbursing independent pharmacies below the Medicaid reimbursement rate. This is the spread pricing problem in statute form. Spread pricing is when a PBM reimburses a pharmacy at one rate but bills the insurance plan or patient at a higher rate, pocketing the difference. It's a practice that exists nowhere except between PBMs and pharmacies. Hospitals don't do it to their suppliers. Insurance companies don't do it to their networks. But PBMs do it to pharmacies, and it's been legal for years. Alabama said: not anymore, at least not for rates below Medicaid.

Second, the law explicitly prohibits steering. Steering is when a PBM directs patients away from a particular pharmacy (often an independent) toward another pharmacy (often a chain or a mail-order operation the PBM owns). Steering is dressed up in language about "network optimization" or "patient convenience," but what it actually means is the PBM chooses which pharmacies succeed and which ones fail based on the PBM's financial interests, not the patient's interests.

Third, Alabama requires 100% rebate pass-through to health benefit plan clients. Rebates are money that drug manufacturers pay to PBMs, supposedly in exchange for formulary placement. The problem is that PBMs have been keeping rebates and not passing them through to the plans that should benefit, which means patients and employers still pay the list price. A requirement for 100% pass-through means the insurance plans and patients actually get the benefit of the rebates that manufacturers are paying for.

And fourth, the law prevents PBMs from denying network participation to pharmacies or retaliating against pharmacies that exercise their legal rights. This sounds vague until you understand that PBMs have historically used network participation as a means of leverage. Pharmacy doesn't accept a lowball reimbursement rate? PBM removes it from the network. Pharmacy joins a trade association that advocates for higher reimbursement? PBM retaliates. Pharmacy sues over underpayment? PBM kicks it off the network. Alabama said: this has to stop.

Each of these provisions addresses a real problem. But here's what matters: Alabama actually enforced them.

The First Enforcement Action (And What It Reveals)

In early 2026, Alabama's PBM Compliance Division, under the supervision of the Department of Insurance, issued a finding against Express Scripts. This was the first enforcement action of its kind in the United States.

The violations were specific. Express Scripts was charging pharmacies illegal fees that weren't part of their network agreements. It was reimbursing pharmacies at rates below the Medicaid reimbursement rate for commercial patients, which is explicitly prohibited by the law. And it was being consistently unresponsive to department inquiries, which is its own kind of violation: if the regulator can't get answers, it can't do its job.

Now here's what I find most important about this enforcement action. It wasn't theoretical. It wasn't based on a formal complaint that the state then spent three years investigating. It was a fairly direct regulatory action based on what the Department of Insurance could observe happening in the marketplace. The state said, "We see the problem. We're enforcing the law. Stop."

Express Scripts doesn't have a mechanism to appeal to a higher authority that might side with the PBM. The law is clear. The violation was documented. The state enforced it.

This changes the incentive structure for PBMs, at least in Alabama. If you violate the law, the regulator will catch you and you'll have to correct the behavior. That's not guaranteed everywhere, but it's guaranteed in Alabama now.

Why This Matters Nationally (And It Really Does)

Here's the part that keeps pharmacy owners awake at night in a good way: this enforcement action creates a template.

For years, PBM reform has been something that pharmacy advocates have talked about in abstract terms. "We need legislation that addresses spread pricing." "We need transparency requirements." "We need enforcement mechanisms." These are the policy goals. But translating policy goals into actual enforcement is where most reform efforts die. The law gets passed, but the regulator doesn't have resources, or appetite, or clarity about how to enforce it. So the law sits on the books and the PBM practices continue.

Alabama proved that this doesn't have to happen. You can write a clear law, establish a compliance division, give that division a mandate to enforce, and actually hold PBMs accountable when they violate. The state didn't need to invent a new regulatory apparatus. It used existing state infrastructure (the Department of Insurance) and gave it a specific focus.

This is replicable. Every state has an Insurance Department. Every state has the legal authority to regulate the entities operating within its borders. Alabama just showed other states how to use that authority.

The national momentum is already building. Other states are watching this. Tennessee is considering similar legislation. Several states are in conversations about what Alabama's law actually accomplished. The pharmacy advocacy world is seeing this as proof that reform isn't just possible, it's achievable in timeframes that matter for business. Not someday. Now.

But here's what matters most: this puts competitive pressure on PBMs. If Alabama enforces its law and Express Scripts has to adjust its behavior in Alabama, it affects Express Scripts' profit model nationwide. PBMs operate with uniform systems across all states. If they can't engage in spread pricing in Alabama, they're going to face pressure to be more transparent about spread pricing everywhere. If they can't steer in Alabama, they're going to be defending their steering practices in other states.

One state's enforcement action creates pressure that ripples across the entire system.

The Express Scripts Specific Issue (And Why It Matters for Your Relationship)

Let me be direct about what Express Scripts was doing, because it illustrates the problem that PBM regulation is trying to solve.

Express Scripts was charging pharmacies fees that weren't contractually agreed to. This is a common practice. A PBM will charge a pharmacy for services, audits, compliance checks, technology fees, without those fees being in the original network agreement. The pharmacy finds out after the fact that their reimbursement was reduced for reasons they didn't know existed. It's a bait-and-switch dressed up in regulatory language.

Express Scripts was reimbursing pharmacies below the Medicaid rate for commercial prescriptions. This is the spread pricing problem. A pharmacy might be reimbursed $15 for a commercial fill while Medicaid would reimburse $18 for the same prescription from the same pharmacy. That $3 spread is spread pricing, and Alabama law explicitly prohibits it. Express Scripts was doing it anyway.

And Express Scripts was blowing off the state's inquiries. When the Department of Insurance asked for documentation about the fees and the reimbursement rates, Express Scripts didn't respond in a timely manner or didn't respond fully. This is where the enforcement action moved from "here are the violations" to "you're also not cooperating with the regulator."

For your pharmacy, if you're an Express Scripts network pharmacy in Alabama, this enforcement action should change your relationship dynamic. You now have a state regulator who has demonstrated that it will enforce the law against the PBM. That changes your leverage. If Express Scripts tries to charge an illegal fee, you have recourse. You have documentation that the state has already told Express Scripts this is prohibited. You can report violations to the Department of Insurance and there's precedent that the state actually investigates.

This is what real PBM accountability looks like, and it starts with enforcement.

What This Means for Pharmacies Outside Alabama

If you're reading this and you're not in Alabama, you might be thinking, "This is interesting but it doesn't affect me." That would be wrong in two important ways.

First, Alabama's law and enforcement action is a toolkit for your state. If you have a state association, you now have evidence that state-level PBM enforcement is possible. You have a specific law to point to. You have data on what Express Scripts and other PBMs are actually doing in your state. You have a template for regulatory language. You have a state (Alabama) that you can ask for advice on implementation.

The pharmacy advocacy world is starting to organize around this. The National Community Pharmacists Association (NCPA) is using Alabama's precedent to pressure other states to pass similar legislation. State associations are looking at Alabama's specific language and adapting it for their own legislatures. This is how policy change actually happens: one state moves first, then others follow.

Second, the Express Scripts enforcement is setting a precedent about what constitutes reasonable enforcement of PBM law. Any pharmacist or pharmacy owner who's been underpaid by a PBM now has an argument to make to their state regulator. "Alabama's Department of Insurance found that Express Scripts was charging illegal fees and reimbursing below Medicaid rates. Our state should investigate whether the same is happening here."

This is where individual pharmacy action connects to systemic change. Every pharmacy owner who files a complaint with their state insurance commissioner is building the case for why enforcement matters. And now there's precedent that regulators can actually do something about it.

How to Advocate for PBM Reform in Your State Right Now

So what should you do if you're an independent pharmacy owner or a tech who cares about this issue?

First, understand the specific PBM problems in your state. Are you seeing spread pricing? Are you being steered? Are you facing fees that weren't contractually agreed to? Document this. Write it down. The more specific you can be, the more persuasive you are when you talk to your state legislator or your state insurance commissioner.

Second, connect with your state pharmacy association. They're organizing around PBM reform. They probably have legislative priorities for this session. Get involved. Even if you're a tech, not a pharmacy owner, your voice matters in these conversations because you're the person who actually sees what PBMs are doing to the dispensing workflow.

Third, if you're seeing PBM violations, report them to your state insurance commissioner. Include specific documentation. Include dates and amounts when possible. Include how the violation affected your pharmacy's finances or operations. The regulator can only enforce the law if they know the violations are happening.

Fourth, if your state has PBM reform legislation pending, testify if you have the chance. Share your specific story about how PBM practices have affected your pharmacy. Policymakers remember personal stories more than they remember statistics. "The PBM reduced my reimbursement by $50,000 this year through fees I didn't know existed" is more powerful than "PBMs are engaging in spread pricing."

And fifth, think about this as an long-term advocacy effort. Alabama's law didn't happen overnight. It took years of advocacy and relationship-building with legislators. But it happened. And now it's a precedent for other states. Your state's PBM reform is the same thing. It's a long-term effort that you're building toward, even if you don't see the policy change this year or next year.

The Diversified Sourcing Reality

Here’s where I want to be honest about what this means for practice right now.

While you’re advocating for PBM reform in your state, you also need to protect your pharmacy’s margins in the conditions that currently exists. And those conditions are still volatile—between reimbursement pressure, contract unpredictability, and ongoing enforcement actions like Alabama’s recent case against Express Scripts , it’s clear that relying on a single channel for margin is no longer a safe strategy. Even national advocacy groups like NCPA are pointing to Alabama as a signal that enforcement is real—but also that pharmacies need to stay resilient while policy catches up.

One of the most practical ways to do that is to diversify your sourcing.

When you’re dependent on a single PBM reimbursement model or wholesaler contract, you’re exposed to sudden margin compression. This is where modern tools—like pharmacy inventory software and a pharmacy-to-pharmacy marketplace—start to play a much bigger role in day-to-day operations.

Platforms like RxPost allow pharmacies to sell excess pharmacy inventory and source medications directly from other pharmacies. That matters more than ever in a world where shortages are unpredictable and overstock turns into loss overnight. Instead of letting products expire on your shelf, you can convert them into revenue—or access inventory another pharmacy no longer needs. It’s a real, operational drug shortage solution that doesn’t depend on upstream fixes.

And the margin impact is real. When you’re sourcing inventory at a discount from another pharmacy instead of through traditional channels, you’re creating a second, independent lever for profitability—one that isn’t dictated by PBM reimbursement rates.

The long-term strategy is still PBM reform and enforcement, like what Alabama is demonstrating. But the near-term strategy is control—control over your inventory, your sourcing, and your margins.

Because the pharmacies that win in this environment won’t just wait for policy to change.

They’ll build businesses that can survive it.

Take Action While You Advocate for Policy Change

Advocacy takes time. Reform takes longer. In the meantime, protect your pharmacy's margins through smarter sourcing. RxPost connects independent pharmacies with surplus inventory at significant discounts, giving you margin flexibility while you're navigating PBM relationships.

Learn how RxPost helps independent pharmacies diversify sourcing and protect margins

Stay Ahead with RxPost Updates

Join our newsletter to receive the latest industry insights, compliance tips, and pharmacy growth strategies straight to your inbox.

Stay Ahead with RxPost Updates

Join our newsletter to receive the latest industry insights, compliance tips, and pharmacy growth strategies straight to your inbox.

Stay Ahead with RxPost Updates

Join our newsletter to receive the latest industry insights, compliance tips, and pharmacy growth strategies straight to your inbox.

Stay Ahead with RxPost Updates

Join our newsletter to receive the latest industry insights, compliance tips, and pharmacy growth strategies straight to your inbox.

Stay Ahead with RxPost Updates

Join our newsletter to receive the latest industry insights, compliance tips, and pharmacy growth strategies straight to your inbox.

RxPost

Obsessed with delivering innovative solutions that maximize efficiencies for a healthier business.

DSCSA

Compliant

Copyright © 2026 RxPost All Right Reserved.

RxPost

Obsessed with delivering innovative solutions that maximize efficiencies for a healthier business.

DSCSA

Compliant

Copyright © 2026 RxPost All Right Reserved.

RxPost

Obsessed with delivering innovative solutions that maximize efficiencies for a healthier business.

DSCSA

Compliant

Copyright © 2026 RxPost All Right Reserved.

RxPost

Obsessed with delivering innovative solutions that maximize efficiencies for a healthier business.

DSCSA

Compliant

Copyright © 2026 RxPost All Right Reserved.

RxPost

Obsessed with delivering innovative solutions that maximize efficiencies for a healthier business.

DSCSA

Compliant

Copyright © 2026 RxPost All Right Reserved.